![]()

ISSN 2379-5980 (online) DOI 10.5195/LEDGER.2023.283

RESEARCH ARTICLE

A Token Economics Explanation for the De-Pegging of the Algorithmic Stablecoin: Analysis of the Case of Terra

Jaewoo Cho *†

![]()

†Jaewoo Cho (jaewoocho@hansung.ac.kr) is Assistant Professor of Social Science at Hansung University, Korea.

*bc1pg96mqcq6daxtudem4p9lgknxns3d5k878zj294sdkuapj5gg705sevlyka

![]()

The recent collapse of Terra has garnered significant attention in the cryptocurrency market. On April 5th, 2022, Terra's native coin, LUNA, reached an all-time high of $119.55. However, on May 13th, its value experienced a drastic decline to $0.00003, representing a decrease of approximately 4 million-fold.1 This “perfect storm” was caused by a de-pegging event of UST.2 UST, also known as TerraUSD, is an algorithmic stablecoin that is integral to the Terra protocol. According to Terra’s whitepaper, UST is a “price-stable and growth-driven” stablecoin, secured by a decentralized protocol and pegged to 1 US Dollar.3 Terraform Labs, the company behind Terra, developed several decentralized financial (DeFi) services based on this promise, including Mirror Protocol and Anchor protocol. Mirror Protocol enables users to create and trade synthetic assets that track the value of real-world assets, while Anchor Protocol allows users to lend and borrow digital assets. These DeFi services attracted a significant number of retail investors, but the collapse of the underlying promise has resulted in significant losses. Many UST holders even hesitated to sell and cut their losses, believing that the situation would return to normal, until the protocol suspended the redemption of UST for LUNA.4

Some have attributed the de-pegging event to a “George Soros-style attack” (a reference to an attack on the value of the British Pound in 1992).5, 6 In this view, an anonymous large entity dumped 85 million UST on a decentralized exchange in an attempt to break the peg, causing fear and a loss of trust among investors and leading others to sell off their UST, thereby accelerating the de-pegging. A recent empirical study focusing on Terra also suggests that a “liquidity pool attack” caused the de-pegging of UST and contributed to the loss of trust in the project, ultimately leading to the catastrophic collapse of both UST and LUNA.7 However, it should be noted that de-pegging events are not uncommon, especially for algorithmic stablecoins that rely on blockchain-level protocols to maintain price stability. Many prior de- pegging events were not the result of a Soros-style attack. There have been theoretical studies arguing that de-pegging is a design flaw inherent in the token economics of stablecoins.8, 9

It is worth noting that there have been theoretical studies examining the importance of token economics design for stablecoins. Calcaterra et al. (2022) identified several “First Order Principles” for stablecoin designs, including burning mechanisms through reserves or bonds, taxation on holding or transactional coins, repegging systems in preparation for black swan events, and governance.10 Other studies have focused on inherent design flaws of algorithmic stablecoins. According to d’Avernas et al.’s 2021 study, collateralization and liquidation protocols play crucial role in crypto-collateral-based stablecoins, and this structure is highly dependent on, as well as vulnerable to, the market liquidity.11 Clements (2021) identifies three fundamental flaws of algorithmic stablecoins: they require a minimum level of demand to run the protocol; they rely on independent arbitrage traders to maintain the pegging mechanism; and they use price information that may not always be trustworthy.12

There are empirical studies supporting the theoretical explanation. Bellia and Schich (2020) review 31 stablecoins, among them 17 algorithmic stablecoins, and found that the prices of algorithmic stablecoins are more volatile than asset-backed stablecoins.13 Cho (2019) also notes that algorithmic stablecoins tend to be more volatile in a strong bear market.8 Earlier algorithmic stablecoins, such as BitUSD, Steem Dollar, and DAI (single-collateral DAI that is an old version of the current multi-collateral DAI), failed to maintain their pegs in the 2018–2020 bear market, and their prices fell from around $1 to $0.5~0.7. Catalini et al. (2021) highlight that a strong bear market switches a fully-backed stablecoin into a partially-backed, and hence holders with fear rush to redeem or sell stablecoins. 14 Saengchote (2021) analyzes this “bank run” of algorithmic stablecoins using the case of Iron Finance, showing that a large number of redeem transactions, particularly “profitable redemptions,” occurred on the blockchain when the stablecoin (IRON) fell from $1 to $0.5.9 Similar analyses by Adams and Ibert (2022) on IRON and Zhao et al. (2021) on Basis Cash also demonstrate that de-pegging is an inseparable problem for algorithmic stablecoins.15, 16

It is worth noting that the de-pegging of stablecoins can be triggered by various factors, such as a bear market and high negative price volatility, a lack of reserves, a loss of trust leading to a bank run, and design flaws in token economics. While these other factors are still important, many empirical studies have pointed out that flawed token economic structures can be a “destined for doom” scheme for algorithmic stablecoins, which can be triggered by arbitrage trading between on-chain redemption and the external markets.9, 11, 12, 14 However, these studies often lack detailed blockchain-level data.

The de-pegging of Terra has garnered attention from both academia and the cryptocurrency industry, as it highlights the potential vulnerabilities of stablecoin systems. This study aims to contribute to the understanding of the causes of the de-pegging of Terra by conducting an in- depth analysis of the token economics of the Terra blockchain. By examining the on-chain data, this study provides insight into the mechanisms behind the de-pegging and how it was driven by the interaction between on-chain redemption prices and market prices. Understanding the underlying causes of the de-pegging of Terra can inform the design and implementation of future stablecoin systems and help prevent similar events from occurring. In the next section, the data and the methodology are discussed, and then the findings and conclusions are presented.

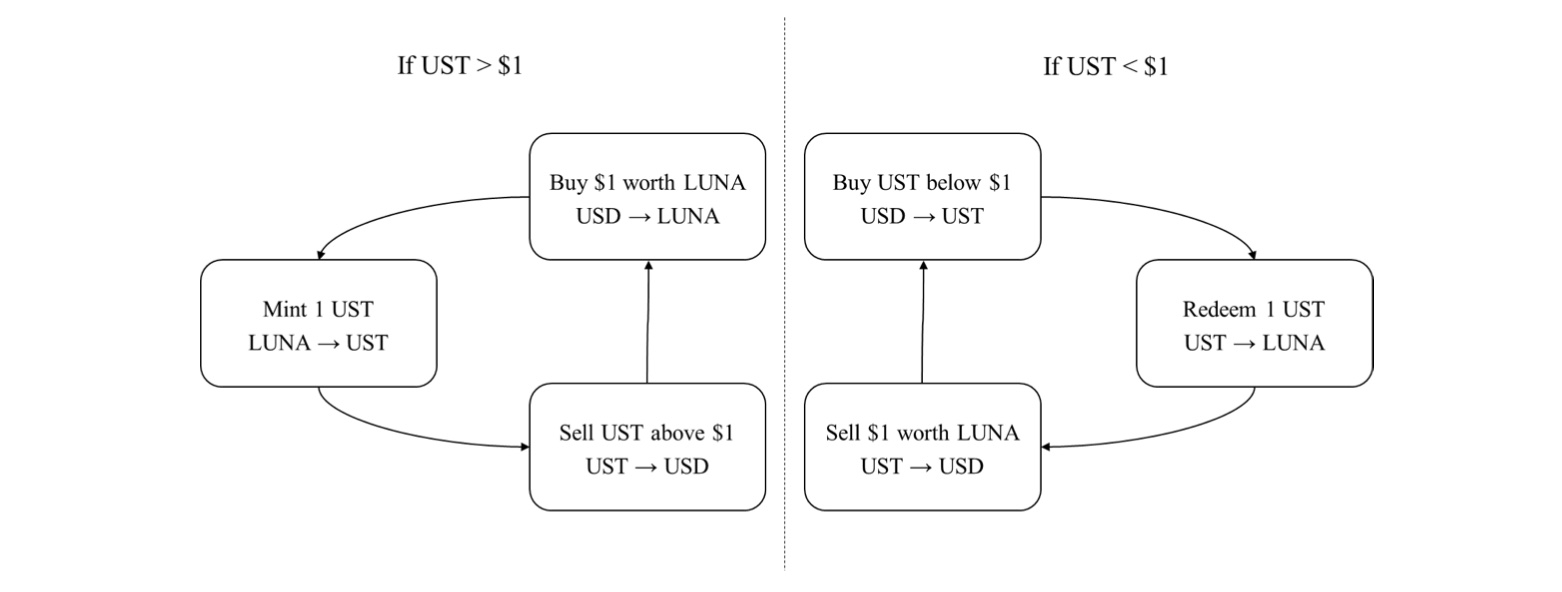

Unlike asset-backed stablecoins that are backed by US dollars, algorithmic stablecoins including UST do not rely on collateral outside of a blockchain. Instead, they use native tokens to mint stablecoins and to guarantee their value. As like other algorithmic stablecoins, users of Terra can mint a unit of stablecoin (UST), by burning a dollar-equivalent LUNA on the blockchain. In addition, whenever they want, they can redeem UST for a dollar-equivalent LUNA. Arbitrage trading plays an important role in keeping the price at the peg, as shown in Figure 1. If the UST price is above the peg, say at $1.10, users can buy $1’s worth of LUNA on crypto exchanges, mint 1 UST with LUNA on the blockchain, and sell it for US dollars at $0.10 profit. If UST is under $1, users can buy cheap UST, redeem UST for $1’s worth of LUNA, and sell and make profits.

Fig. 1. Arbitrage trading processes for UST pegging.

This works effectively in a bull market, where the value of the stablecoin remains relatively stable. However, the fragility of this mechanism becomes evident in a bear market, when the value of the stablecoin may decrease steadily or rapidly. In this situation, a de-pegging event can occur in two ways.

Firstly, UST holders may expect that the stablecoin will not be fully redeemed in fiat terms for various reasons, such as delays in transferring tokens from the Terra blockchain to cryptocurrency exchanges, or protocol-level haircuts in redeeming the stablecoin due to the market cap of the collateral currency (in this case, LUNA) being less than the market cap of the stablecoin, UST. Secondly, the highly volatile price brings about greater uncertainty, then arbitrage traders want to buy stablecoins below a dollar to secure a safe margin, which brings about the de-pegging in the market. Focusing on the former reason, this study examines whether undercompensation of UST leads to the de-pegging event.

This study aims to examine whether undercompensation of UST leads to de-pegging events, with a focus on the first reason mentioned above. By analyzing the relationship between undercompensation and de-pegging events, this research aims to contribute to the understanding of stablecoin mechanisms and their potential vulnerabilities in bear markets.

A key part of this study is on-chain analysis using blockchain-level data. Specifically, “swap” transactions to convert UST to LUNA are important data for investigating the de-pegging mechanism. Terra has three sources of swap data: on-chain market, Terraswap, and Astroport. Of these three sources, the on-chain market data is the most essential because the swap ratio is determined solely by the Terra blockchain protocol and is not influenced by the UST price on exchanges. This means that the blockchain always assumes the UST price is $1, regardless of whether the market price is above or below that value. The remaining two sources, Terraswap and Astroport, are also blockchain transactions, but they are decentralized exchanges based on smart contracts on the Terra blockchain. As a result, the swap ratio in these sources is not determined by the Terra protocol, but rather by market players. In practice, Terra Station, Terra's swap service, automatically suggests the best price among these three sources to traders. This study analyzes three types of swap transactions on the Terra blockchain during the period when the de-pegging event occurred until the swap function was removed. The analysis covers the time period from block 7562591 (May 9, 2022 00:00:05 UTC) to block 7607789 (May 13, 2022 01:58:49 UTC) (Terra, 2022).17

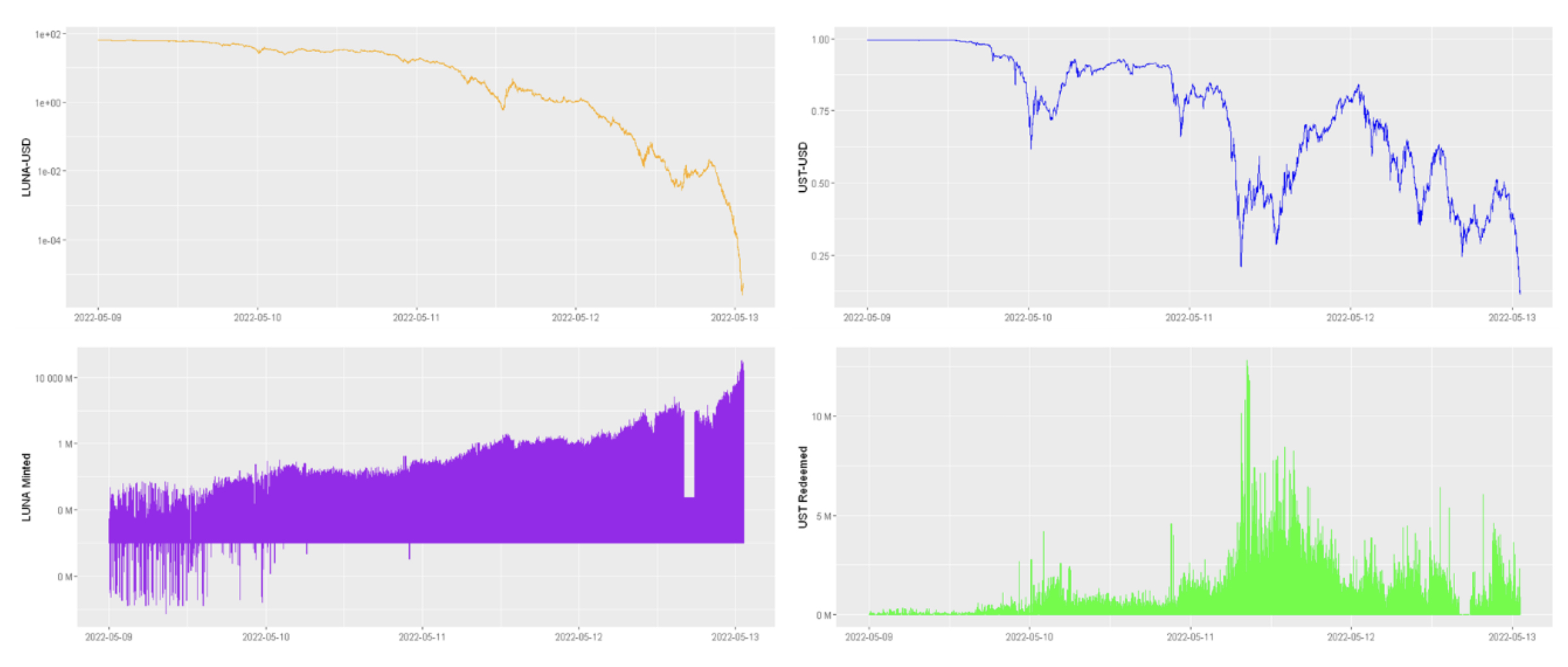

For the market data, the prices of UST–USD and LUNA–USD pairs on the FTX exchange are collected via tradingview.com. Considering the high-volatility and high-frequency nature of cryptocurrency trading, the closing price at every minute is used. This study aggregates the amounts of swapped UST and redeemed LUNA to one-minute windows to match the market data. Then, it calculates the LUNA-to-UST ratio, and the ratio is multiplied by the LUNA–USD market price, assuming that redeemed LUNA can be sold on exchanges to obtain USD. The resulting swapped value of UST is then calculated. Table 1 presents descriptive statistics of the data and Figure 2 illustrates price history of LUNA and UST and minted and redeemed amounts of LUNA and UST. The patterns imply relationships between LUNA price and minted amount, and between UST price and redeemed amount.

Table 1. Descriptive statistics.

Obs. | Mean | Median | Min. | Max. | |

UST Price | 5833 | 0.7401 | 0.7911 | 0.1117 | 0.9960 |

LUNA Price | 5833 | 22.45 | 15.83 | 2.5e-06 | 65.12 |

Redeemed Value | 5833 | 0.7926 | 0.8336 | 0.0587 | 1.6874 |

Spread | 5833 | 0.2073 | 0.1664 | -0.6874 | 0.9413 |

Fig. 2. Price history of LUNA (top-left) and UST (top-right), minted amount of LUNA (bottom-left), and redeemed amount of UST (bottom-right).

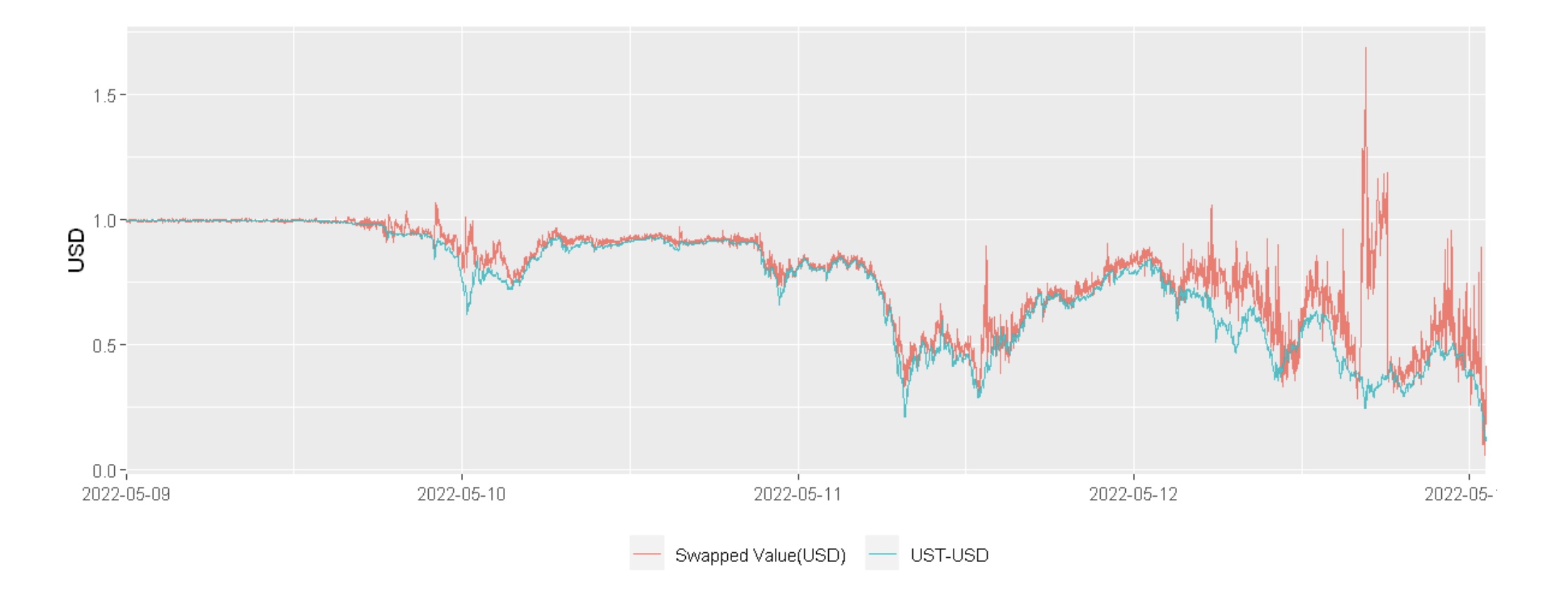

This study calculates the redeemed value in USD per UST and compares the redeemed value and the UST price on the exchange, as shown in Figure 3.

Fig. 3. Comparison between the swapped value of UST and UST–USD on the exchange, 9 May to 12 May.

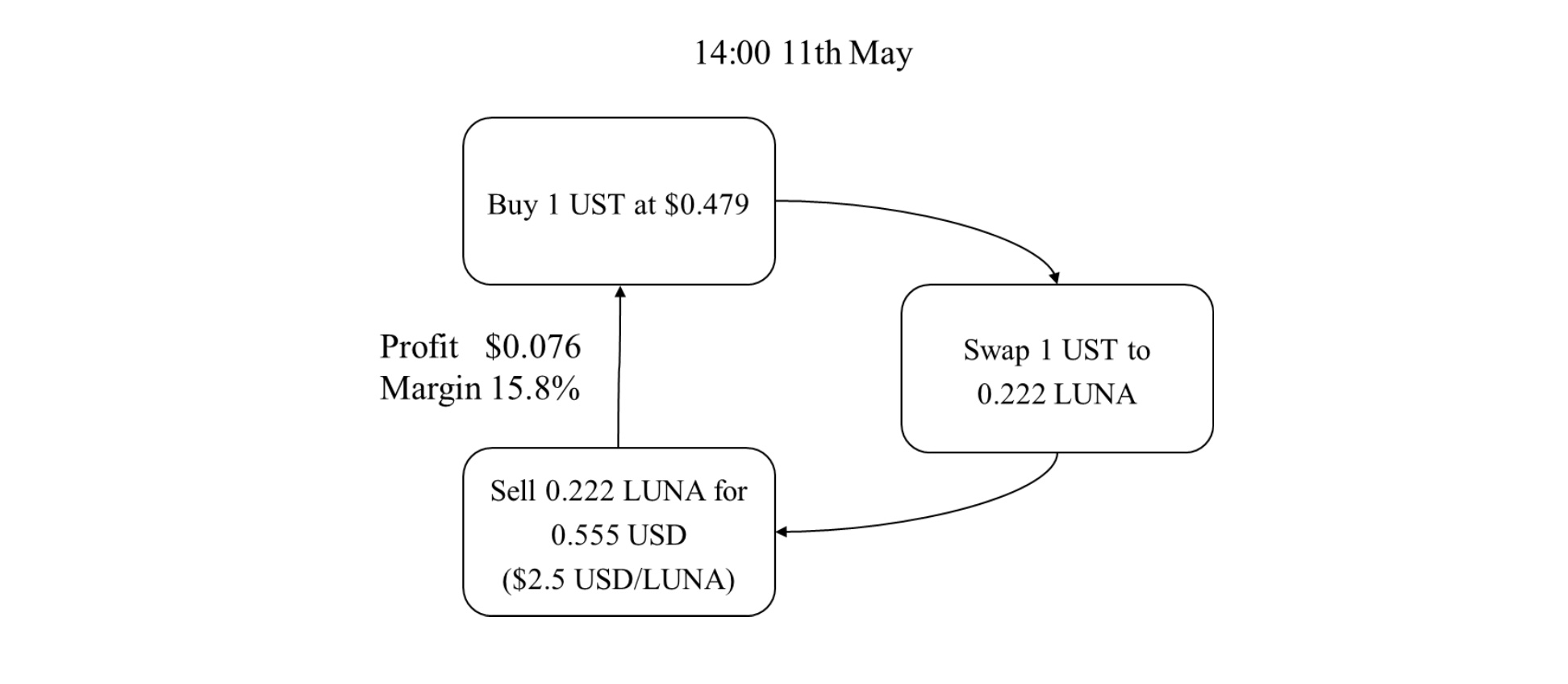

The two lines in Figure 3 move very closely together. There is a strong correlation between the UST price and the swapped value, with a correlation coefficient of 0.955. However, as shown in the figure, the redeemed value appears to be greater than the UST price in most observations. Specifically, 81.5% of observations have a greater swapped value than UST price. In this situation, arbitrage traders can profit by buying cheap UST (UST–USD) and executing a “swap and sell” at a higher price. Additionally, it can be interpreted that arbitrage traders are sufficiently rational that they do not want to buy UST at a value higher than the profit they can acquire by swapping UST to LUNA. For example, at 14:00 on May 11, arbitrage traders could earn $0.076 per UST, or a 15.8% margin, using this process (Figures 4 and 5).

Fig. 4. Difference between swapped value and market price of UST.

Fig. 5. An example of arbitrage trading at 14:00 on 11 May.

This arbitrage activity is normal and expected, as it helps to secure the pegging. By purchasing and burning UST, the demand for UST increases while the supply decreases, leading to an increase in the price of UST to $1. If the blockchain always redeems $1 worth of LUNA for UST holders, the peg would be recovered. However, from the perspective of token economics, the de-pegging event continued. What could be the possible reason for this?

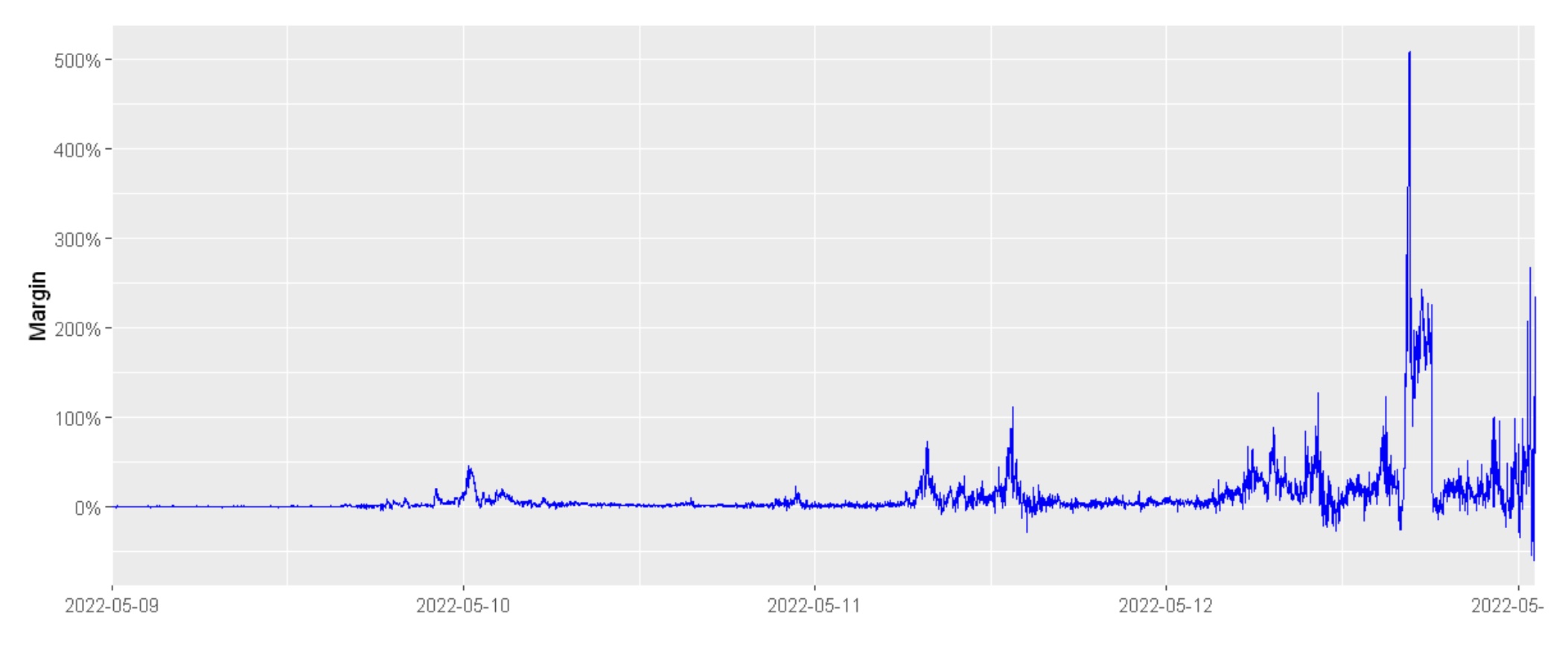

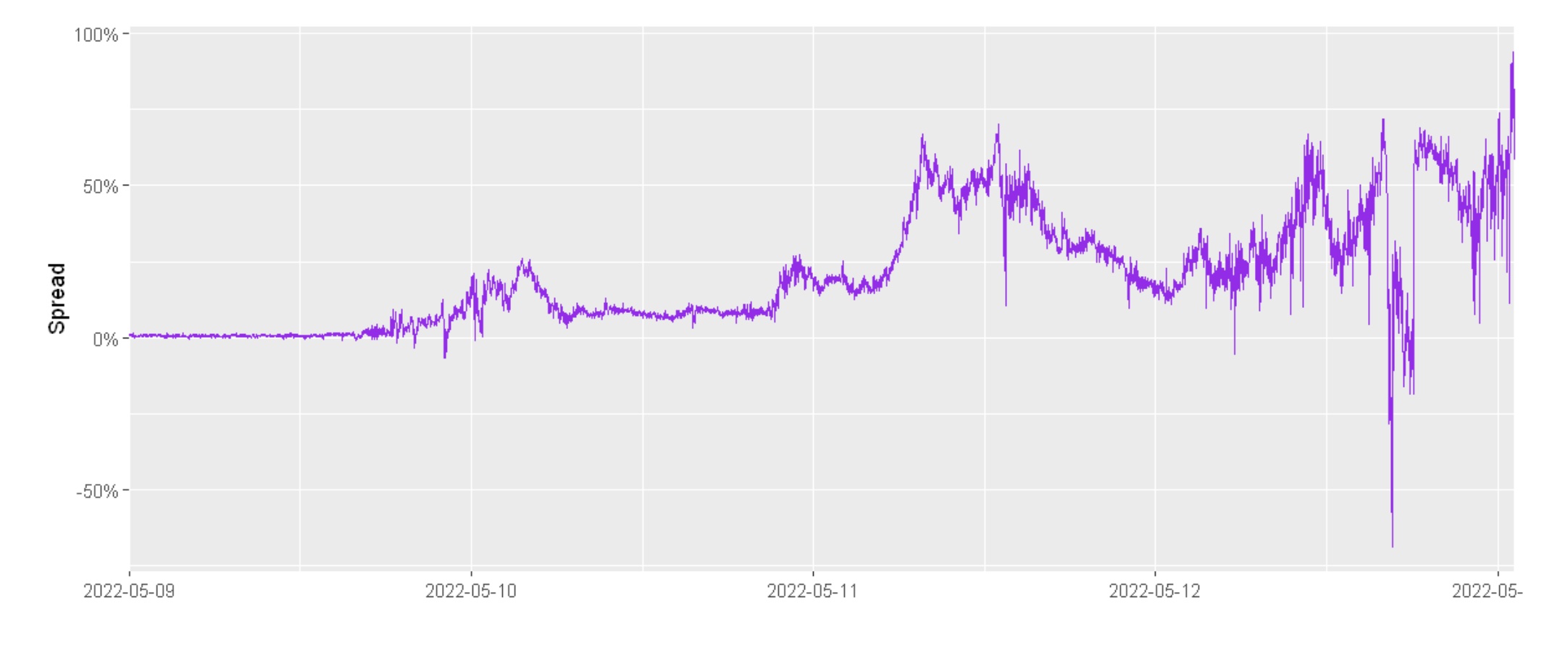

The Terra blockchain has a virtual liquidity pool for the UST-LUNA pair.18 This system operates similarly to UniSwap, using a Constant Product market.19 When users swap a large amount of UST, meaning that they send UST to the pool and withdraw LUNA from it, the pool becomes imbalanced and lacks LUNA. In this case, the blockchain protocol penalizes the UST- to-LUNA swap by setting a higher spread, causing UST to be swapped for less than $1. During the de-pegging event, the effective spread reached up to 94.1%, with an average of 20.7% and a weighted average of 31.9% (Table 1, Figure 6). This means that UST is redeemed significantly below $1. Given that UST is undercompensated, rational market players do not want to buy UST at higher prices than the redeemed values on the blockchain.

Fig. 6. Spread on swap transaction set by Terra blockchain.

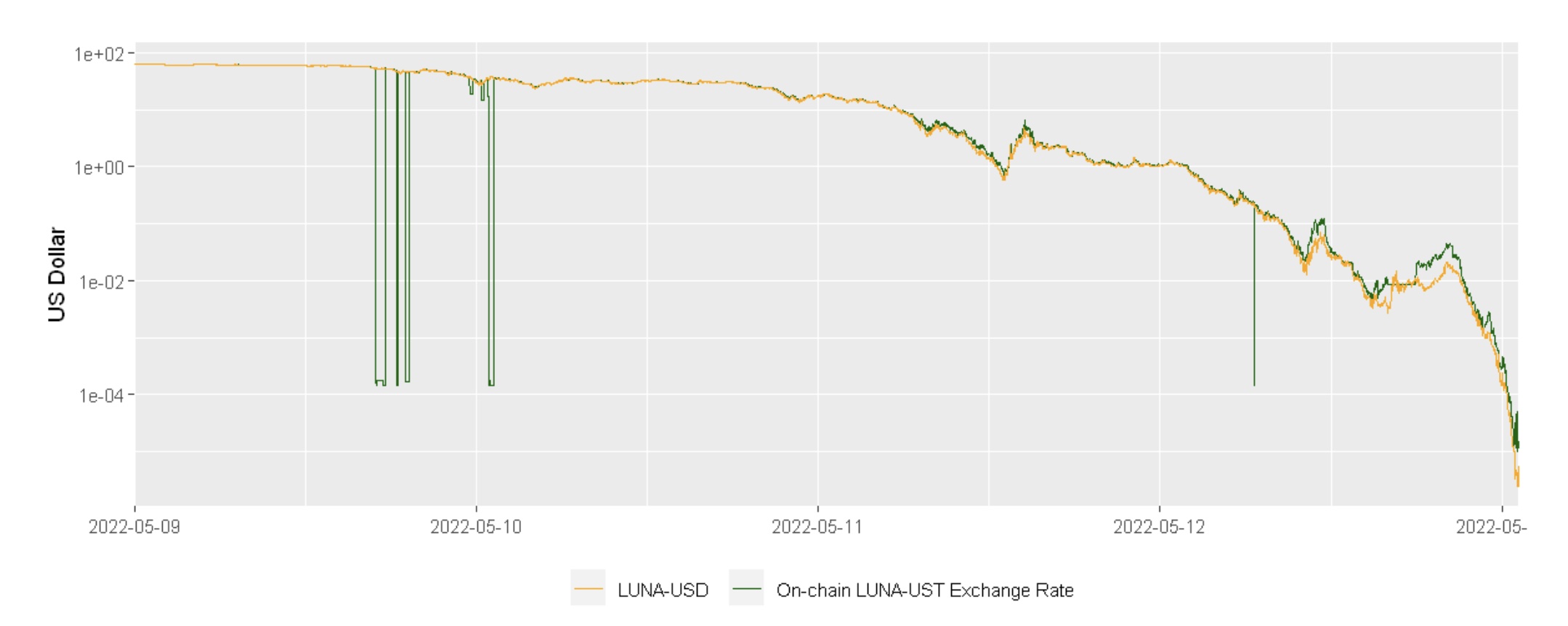

It is worth noting that the on-chain exchange rate between LUNA and UST set by Terra’s oracle, which is provided by block validators in a decentralized way, moved along with LUNA_USD price on exchanges (Figure 7). This means that the Terra blockchain was assuming UST as $1 during the de-pegging event. If Terra had taken the de-pegging into account, the exchange rate should have been significantly higher than the market price. For example, if UST is discounted by 50%, to $0.5, and LUNA is valued at $50, the LUNA-UST exchange rate should be 100. However, this was not the case. This suggests that the undercompensation was not due to external factors, such as market price, but was instead related to an internal mechanism of token economics.

Fig. 7. On-chain LUNA-UST exchange rate and LUNA-USD market price.

This study attempts to examine the causal relationship between the swapped value and the UST price. Theoretically, the swapped value should not be affected by the UST price on exchanges because the blockchain always assumes a constant UST value of $1, as mentioned previously. However, the market price can be influenced by the redeemed value due to arbitrage trading. To analyze this relationship, this study employs Granger causality analysis. Table 2 shows the results using the first differences of the redeemed value and UST price.

While the impact of swapped value on market price is consistent across different lag, from one to ten minutes, the market value has no significant effect on swapped value at the 5% statistical level between four to nine minutes. This unidirectional relationship supports the theoretical hypothesis and implies that the swapped value of UST, which is guaranteed by the blockchain, tends to change the market price of UST, especially during the de-pegging event.

Table 2. Results of Granger causality analysis.

| p-value | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Lag (min.) | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Swap → Market | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 | <0.001 |

| Market → Swap | <0.001 | <0.001 | 0.007 | 0.126 | 0.094 | 0.245 | 0.400 | 0.833 | 0.208 | 0.037 |

The de-pegging of stablecoins, such as Terra, can have significant consequences for both users and market participants. It is important for researchers and practitioners to understand the underlying causes of such events in order to inform the design and implementation of future stablecoin systems and prevent similar occurrences. The present study aimed to contribute to this understanding by conducting an in-depth analysis of the token economics of the Terra blockchain during the de-pegging event. By examining the on-chain data, this study was able to provide insight into the mechanisms behind the de-pegging and how it was driven by the interaction between on-chain redemption prices and market prices.

The contribution of the present study is the examination of the role that the economics structure of the Terra blockchain protocol and the rational decision-making by market participants played in the de-pegging event. The analysis suggests that the misdesigned redemption structure of the UST was a key factor in the de-pegging, with the “attack” serving as a trigger for the dynamics arising from the flawed design. The real attack was carried out by market participants taking advantage of the opportunity for arbitrage trading. In order to design effective, sustainable, and secure blockchain protocols, it is crucial to carefully consider the token economics structure and potential scenarios.

This work is financially supported by Hansung University.

1 Messari. “Historical Data for Terra Luna Classic.” Messari.io (accessed 22 December 2022) https://messari.io/asset/terra-luna-classic/historical/.

2 Malwa, S. “Terra-Based DeFi Protocol Anchor Proposes Cutting UST Yield Rates to 4%.” Coindesk (accessed 27 May 2022) https://www.coindesk.com/markets/2022/05/12/terra-based-defi-protocol-anchor-proposes-cutting-ust-yield-rates-to-4.

3 Kereiakes, E., Kwon, D., Di Maggio, M., and Platias, N., “Terra Money: Stability and Adoption (version 1.1)” (accessed 19 March 2023) https://whitepaper.io/document/587/terra-whitepaper.

4 Uhlig, H. “A Luna-tic Stablecoin Crash.” National Bureau of Economic Research (working paper 30256) (July 2022) https://dx.doi.org/10.3386/w30256.

5 Volpicelli, G. “Terra’s Crypto Meltdown Was Inevitable.” Wired (12 May 2022) https://www.wired.com/story/terra-luna-collapse.

6 Mallaby, S. “Go for the Jugular.” The Atlantic (2010) https://www.theatlantic.com/business/archive/2010/06/go-for-the-jugular/57696/.

7 Briola, A., Vidal-Tomás, D., Wang, Y., and Aste, T. “Anatomy of a Stablecoin’s Failure: The Terra-Luna Case.” Finance Research Letters 51 103358 https://doi.org/10.1016/j.frl.2022.103358.

8 Cho, J. “The Present and The Future of Stablecoins.” FIRIC Issue Paper No. 1, Korea Advanced Institute of Science and Technology (accessed 19 March 2023) https://kpc4ir.kaist.ac.kr/?module=file&act=procFileDownload&file_srl=2801&sid=b 4220705722ad98ec409dc00c8c143ce&module_srl=2315.

9 Saengchote, K. “A DeFi Bank Run: Iron Finance, IRON Stablecoin, and the Fall of TITAN.” SSRN (accessed 19 March 2023) https://dx.doi.org/10.2139/ssrn.3888089.

10 Calcaterra, C., Kaal, W. A., & Rao, V. “Stable Cryptocurrencies: First Order Principles.” Stanford Journal of Blockchain Law & Policy 3 62 (5 January 2022) https://stanford-jblp.pubpub.org/pub/stable-cryptocurencies-principles.

11 d’Avernas, A., Bourany, T., & Vandeweyer, Q. “Are Stablecoins Stable?” Banque de France Working Paper (accessed 19 March 2023) https://particuliers.banque-france.fr/sites/default/files/media/2021/06/10/gdre_bounary.pdf.

12 Clements, R. “Built to Fail: The Inherent Fragility of Algorithmic Stablecoins.” Wake Forest Law Review Online 11 131 (accessed 19 March 2023) http://www.wakeforestlawreview.com/2021/10/built-to-fail-the-inherent-fragility-of-algorithmic-stablecoins/.

13 Bellia, M., and Schich, S. “What Makes Private Stablecoins Stable?” SSRN (26 October 2020) https://dx.doi.org/10.2139/ssrn.3718954.

14 Catalini, C., de Gortari, A., and Shah, N. “Some Simple Economics of Stablecoins.” SSRN. MIT Sloan Research Paper 6610-21 (20 December 2021) https://dx.doi.org/10.2139/ssrn.3985699.

15 Adams, A., and Ibert, M. “Runs on Algorithmic Stablecoins: Evidence from Iron, Titan, and Steel.” FEDS Notes (2 June 2022) https://www.federalreserve.gov/econres/notes/feds-notes/runs-on-algorithmic-stablecoins-evidence-from-iron-titan-and-steel-20220602.htm.

16 Zhao, W., Li, H., and Yuan, Y. “Understand Volatility of Algorithmic Stablecoin: Modeling, Verification and Empirical Analysis.” In M. Bernhard et al. (Eds.) FC 2021: International Conference on Financial Cryptography and Data Security 97-108 (17 September 2021) https://dx.doi.org/10.1007/978-3-662-63958-0_8.

17 Terra (@terra_money). Twitter post. Twitter (13 May 2022). Original post deleted, available via the Wayback Machine: https://web.archive.org/web/20220513124703/https://twitter.com/terra_money/status/1525095111389945857. [Tweet reads (in full): “The Terra blockchain has resumed block production. Validators have decided to disable on-chain swaps, and IBC channels are now closed. Users are encouraged to bridge off-chain assets, such as bETH, to their native chains. Note: Wormhole bridge is currently unavailable.”]

18 Terra Docs. “Terra Core Modules – Market.” (accessed 22 December 2022) https://classic-docs.terra.money/docs/develop/module-specifications/spec-market.html.

19 Adams, H., Zinsmeister, N., Salem, M., Keefer, R., and Robinson, D. “Uniswap v3 Core.” uniswap.org (accessed 19 March 2023) https://uniswap.org/whitepaper-v3.pdf.