![]()

ISSN 2379-5980 (online) DOI 10.5195/LEDGER.2023.288

REVIEW ARTICLE

Blockchains and Triple-Entry Accounting for B2B Business Models

Muhammad Imran Sarwar,∗ Kashif Nisar,† Imran Khan,‡ Danish Shehzad§

![]()

∗1HS1e1aQvTCWiRWiCyedF5hpAcj4GhzaXQ

† M. I. Sarwar (info@imranchishty.com) and K. Nisar (qashef@gmail.com) are PhD Candidates in the Department of Computer Science & IT at The Superior University, Lahore, Lahore-54500, Pakistan.

‡ Dr. I. Khan (imrankhan@superior.edu.pk) is an Assistant Professor in the Department of Computer Science & IT at The Superior University, Lahore, Lahore-54500, Pakistan.

§ Dr. D. Shehzad (danish.shehzad@superior.edu.pk) is an Associate Professor in the Department of Computer Science & IT at The Superior University, Lahore, Lahore-54500, Pakistan.

![]()

B2B (business-to-business) refers to commercial transactions between two or more businesses and can involve the sale of goods, services, or information between businesses.1 B2B transactions are common in various industries, including manufacturing, wholesale, and professional services. With technological advancement and high-speed internet availability, B2B has expanded from a local to an international marketplace.2 B2B transactions are typically characterized by higher volumes, larger transaction sizes, and longer sales cycles than B2C (business-to-consumer) transactions. B2B sales often involve business negotiations and may require customized solutions to meet each customer’s needs. Overall, B2B transactions play a critical role in the global economy, facilitating the exchange of goods, services, and information between businesses and driving economic growth and innovation.3

Double-entry accounting has been the standard method of recording financial transactions for centuries, and it remains a fundamental part of accounting practices today. However, there are limitations to double-entry accounting.4 In this technological age, technological progress is swift. People and businesses are becoming more demanding and seeking optimized solutions to meet their needs and overcome day-to-day obstacles.5 The same scenario holds true for bookkeeping activities that directly assist management and decision-making, such as record- keeping and reporting.6 Modern Accounting Information Systems (AIS) are deployed using Enterprise Resource Planning (ERP), which provides an environment and logically expands the AIS’s functionality across the organization.7

Several centuries ago, DEA principles were used in the AIS and have not been challenged for effectiveness. Accounting books prepared by a company using DEA are trustworthy and reliable, but the trustworthiness is never convincing for other companies. When it comes to huge transactions and large businesses, the DEA lacks credibility. Two companies record business transactions in their books, which they use and value.8 Records managed using DEA can be vulnerable to fraud and errors, particularly if they are stored in paper form or on unsecured computer systems. While double-entry accounting remains a fundamental part of accounting practices, it has limitations, particularly in B2B transactions.

The term Triple-Entry Accounting coined in 1986, is a logical expansion of DEA and relies on three accounting entries. Since then, TEA has become a hot topic for researchers and financial experts as to how and to what extent it addresses the limitations of DEA.9 The concept of a shared or distributed ledger in TEA via a blockchain is the same and works identically because the third entry is considered a logical part of the other two entries.10 The recording of the third entry in TEA or a blockchain is a kind of witness entry, and it caters only to those transactions in which any outside person or business is involved. Such transactions include sales, collections, purchases, payments, etc. For any internal business transaction, there is no role for TEA, as they are entered in the internal accounting books and do not have an obligation to any external person or party. Examples of such transactions are selling and shipping expenses, general and administrative expenses, income other than sales, etc.

Objective of the Study—Limited research on blockchains and TEA-based applications and their use in B2B business is available. This study aims to survey the current state of adaptation and implementation of blockchains and TEA concerning B2B transactions from the available literature and also discuss the potential opportunities and challenges of implementing TEA through blockchains for B2B transactions. We have also analyzed some case studies on blockchains and TEA-based commercial applications. This study seeks to fill the gap by elaborating on the existing work on the topic. Subsequently, this research paper analyzes how blockchains and TEA can address the limitations of DEA regarding their implementation in the B2B business model. Our findings would deepen our understanding of blockchains and the use of TEA in B2B transactions, as they would identify new opportunities and challenges.

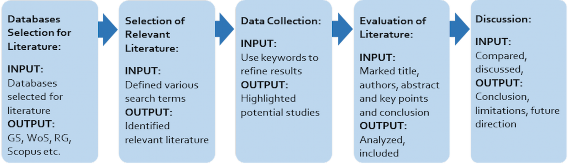

Research Methodology—The research methodology used in this study can be classified as exploratory qualitative analysis. It surveys some of the latest studies on adopting and implementing blockchain-based TEA in the B2B business model. The analysis of the published literature, on which this research is based, can be divided into two distinct groups: 1) studies that proposed and discussed three accounting entries of an accounting transaction; and 2) studies that highlight the potential of blockchains in the accounting, finance, and audit domains. Different scientific databases were explored to search for relevant literature. Various terms were used to find the material, including “triple-entry accounting,” “Blockchain and triple-entry accounting,” “advantages and limitations of double and triple entry accounting,” “Blockchain and triple-entry accounting for B2B transactions,” “limitation of double-entry accounting in B2B business,” “trust issues in B2B business” and “opportunities and challenges using Blockchain in B2B business.” After screening, we only selected papers that had been published in reputable journals and conference proceedings in the recent past. Figure 1 illustrates the steps involved in the research methodology.

Fig. 1. Research methodology: step-by-step.

Structure of the Article—The rest of the paper is structured as follows: Section 2 presents the background of blockchains, accounting models, and B2B business. Section 3 covers a literature review on the evolution of bookkeeping, SEA, DEA, the three theories of TEA, blockchains for accounts, finance and audit, and blockchains, trust and B2B business. Section 4 is on the discussion and key findings in the literature. Finally, Section 5 summarizes the study’s conclusion and possible future directions.

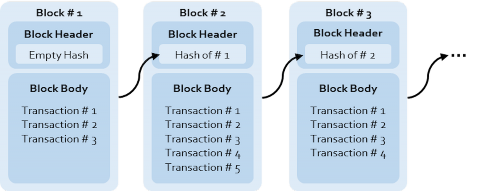

Blockchains—Blockchains, since their inception, have been in the spotlight, and in recent years, we have seen them among the top-ranked technologies in the IT domain. Since blockchain data is shared between nodes in a distributed network, it cannot be altered once it has been recorded.11 The entire chain of blocks is distributed across the network; therefore, any deletion or alteration in the data becomes nearly impossible, ensuring the data’s immutability and transparency. Blockchains store data in blocks that are securely linked together. Strong cryptographic primitives, such as SHA (secure hash algorithms), are at the core of the blockchain and are used to couple the blocks together to guarantee data integrity.

Though other developments preceded it, the first decentralized blockchain was introduced in 2008 with Bitcoin, a digital currency; it was the first decentralized application without any trusted third parties.12 At that time, the technology was developed as the foundation of Bitcoin. It has become evident that blockchains may be implemented in different domains other than cryptocurrencies due to their numerous characteristics, such as confidentiality, immutability, one-way transactions, and openness. These unique characteristics distinguish blockchains from conventional data storage technologies like RDBMS. Despite technological obstacles and advances in technology and hardware, blockchains continue to assert their immaculate nature due to cryptographic primitives.13 The structure of the Bitcoin Blockchain is illustrated in Figure 2.

Fig. 2. Structure of a blockchain.

Accounting Models—Bookkeeping has evolved over thousands of years, from simple methods of keeping track of goods and trade transactions in ancient civilizations to modern accounting software and computer-based recordkeeping systems. In ancient times, traders and merchants kept track of their transactions on clay tablets or papyrus scrolls. The earliest known recordkeeping systems date back to around 2600 BCE in Mesopotamia and Egypt.

Fig. 3. Double-Entry bookkeeping in Alice’s books.

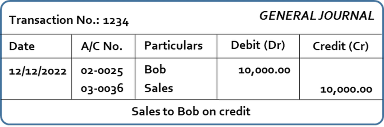

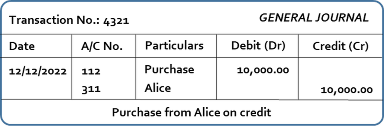

Accounting had a crucial technical function in developing rationality and advancing the evolution of capitalist production systems.14 One of the most significant evolutionary achievements in accounting history was the conception of ”double entry” and its eventual transformation.15 DEA is a scientific method for maintaining financial records based on the duality concept. Each transaction simultaneously affects two accounts, one receiving a debit and the other a credit. Due to its dual effects while documenting transactions in books, the DEA system is efficient and comprehensive. The DEA concludes the final accounts with an income statement and a balance sheet, beginning with the journal entry and progressing through the ledger and trial balance.16Figures 3 and 4 show examples of a double-entry accounting entry of the sales and purchases on credit in Alice’s and Bob’s books, respectively.

Fig. 4. Double-Entry bookkeeping in Bob’s books.

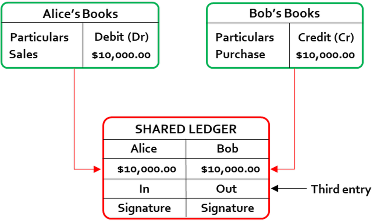

The term Triple-Entry Accounting was introduced by an accounting scholar, Yuji Ijiri, in 1986. In addition to debit and credit, he proposed the “trebit” and conceptually added another layer to the DEA.17 In a financial transaction involving two parties, they record the transaction in their books and endorse it as a giver and receiver in the shared ledger. A white paper on TEA was published in 2005 by financial cryptographer Ian Grigg, who presented a very different conception of TEA than Ijiri. Grigg argues that “the receipt is the transaction,” since it is digitally or cryptographically signed and recorded in a public ledger that can be viewed by both parties.18 The key difference between TEA and DEA is that TEA can elevate public trust toward more trustworthy and transparent systems because it prevents manipulating electronic data. 19 DEA has been the standard method of recording financial transactions for centuries. In contrast, TEA with a blockchain provides an additional layer of transparency and security to the accounting process, allowing all parties involved in the transaction to access and verify the same information in real time. Figure 5 shows an example of recording transactions between Alice and Bob in their respective books and the third entry in a shared ledger.

Fig. 5. Triple-Entry bookkeeping.

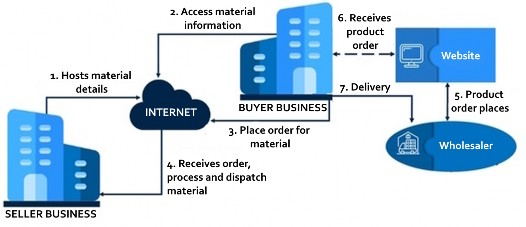

B2B Business Model—B2B transactions are typically characterized by higher volumes, larger transaction sizes, and longer sales cycles than business-to-consumer (B2C) transactions. B2B sales often involve business negotiations and may require customized solutions to meet each customer’s needs. B2B transactions play a critical role in the global economy, facilitating the exchange of goods, services, and information between businesses and driving economic growth and innovation. Due to the large volume of transactions and the huge number of sellers and buyers, trust-related issues remain critical in this type of business model. One of the primary trust issues is a lack of information, as every party needs to know enough about the other to feel comfortable before entering into a business deal. One party may misrepresent its products or services, delivery times, pricing, and payment terms to gain an advantage over the other party. Failure to pay or late payment can damage trust between parties, especially if it happens repeatedly. Lack of communication between parties can lead to misunderstandings and mistrust, and fraudulent practices cannot be ignored. Figure 6 depicts a B2B business model between two parties, the buyer and the seller.

Fig. 6. B2B business model.

Single-Entry Accounting (SEA)—SEA is considered the oldest bookkeeping method, used since ancient times, in which transactions are recorded in a single column. This is a simple and straightforward method that is perfectly suitable for small businesses and individuals with no particular requirements. Transactions are recorded in a cash book with some additional information like the transaction date, amount, and a brief description. SEA is mostly supportive and helpful in recording transactions related to cash, receivables, payables, and expenses.20 Although SEA is a quite simple accounting method, it has several limitations. One of the major problems is that it does not reflect the real-time position of the business as some critical information like assets and liabilities is not recorded; therefore, it doesn’t help in decision-making. Even though the SEA method of accounting is fairly straightforward, it does have a few drawbacks. One of the most significant issues is that it does not accurately reflect the current position of the company because essential information such as assets and liabilities is not recorded; as a result, it does not assist in the process of decision-making. Because there is no cross-verification of accounts like there is in the DEA, there is a significant risk that errors and fraudulent activity will go unnoticed. The majority of its users were sole proprietors, manufacturers and individuals. It is still used on a smaller scale, where there are no mandatory or complex reporting requirements.21 It has almost completely been replaced with DEA for more up-to-date and detailed reporting as a result of the complexity of business operations and the

demands placed on modern businesses.

Double-Entry Accounting (DEA)—DEA, developed in the 15th century, is a systematic method to record accounting transactions. It is a revolutionary method of bookkeeping that introduces the concept of dividing a transaction into two dimensions and recording them as debit and credit. One part of the transaction gets debited and the other gets credit, which also balances the two sides and helps prevent errors and fraud.22 The 20th-century industrial revolution transformed manufacturing processes and introduced new approaches to trade and commerce. More efficient and advanced bookkeeping methods were required to handle business operations and financial reporting, which led to the development of new costing and budgeting accounting systems, and DEA was able to support the new requirements. Later, with the emergence of computer-based accounting and financial applications, the entire paradigm of bookkeeping was shifted. This technological advancement made bookkeeping more fast, accurate, and effective.23

Three Entries by Fedor Esersky—In 1878, a Russian scholar Fedor Esersky first time proposed the idea of recording an accounting transaction with three entries. He highlighted some shortcomings in DEA and suggested recording three entries in three different books, 24, 25 and his proposed accounting model is therefore called “Russian Triple-Entry.” Esersky contended that with DEA, it was not possible to gain precise enough insights into a business, and to address this issue, he proposed three accounting entries in three accounting books: 1) a chronological book for recording transactions in the order they occur; 2) a systematic book for recording all transactions; and 3) a balance sheet book to record a summary of all transactions. The researcher believed that a transaction must be recorded after its completion. The key idea was passing three entries in three books; therefore, it would be more appropriate to call “Russian-Triple-Entry” instead by the name “Triple-Book Entry.” Although three entries are required to record a transaction, this concept contradicts the understanding of TEA presented in recent years.

Triple-Entry Bookkeeping by Yuji Ijiri—The term “Triple-Entry Bookkeeping” was introduced by a Japanese accounting scholar, Yuji Ijiri, in 1986.17 Ijiri claimed that double-entry bookkeeping was not extendable. Still, logically, it is possible, and he presented a relationship between income and wealth. He claimed that wealth differed from income and introduced the idea that “the rate at which the income is being earned” or “the rate at which the wealth is changing” could be called “momentum,” which could be measured in monetary units and over a specific time. He called his model “momentum accounting,” and it deals with three types of accounting: wealth, momentum and force. In addition to debit and credit, he named the third accounting entry “tribit” and highlighted the importance of the change in momentum and its impact on wealth for a specific period. A closer look at the concept of Ijiri’s Triple-Entry bookkeeping reveals that the third entry has nothing to do with the conceptual workings of blockchains. The proposed model was not to support a third or witness entry in a distributed or common ledger but to record the transactions to present a real-time output in financial terms.

Triple-Entry Accounting by Ian Grigg—In 2005, the concept of TEA was revamped by Ian Grigg in a working paper.18 The author, a financial cryptographer, presented a different concept of TEA. He claimed that a receipt signed cryptographically could be a challenge to double-entry bookkeeping, and a digital signature made via financial cryptography would strengthen the whole system manyfold. The study further claimed that if accounting expanded in the digital cash domain, it would give three transactions, two local and one logical, for each of the three roles, and resultantly, should be called TEA. This concept of TEA differs from what Esersky and Ijiri presented. Grigg presented the concept of TEA by combining cryptography and bookkeeping. He described his model as “recordkeeping for two or more parties through a shared transaction repository (STR) with a signature by all parties.” Once all parties cryptographically sign a transaction, it is sent to a DL and then distributed to the respective ledgers of the concerned parties. Further, a digitally-signed transaction with due authorization could challenge the DEA. The digital signature is strong digital evidence that solves the parties’ reconciliation issues by sharing the transaction with each party as evidence.

Grigg’s TEA is best described with an example. As depicted in Figure 5 (above), a transaction takes place between Alice and Bob, where Alice sells some goods to Bob worth $10,000. Alice and Bob will record the transaction in their respective books in DEA, as shown in Figures 3 and 4, where Alice debits Bob against the sales of goods and Bob credits Alice against the purchase of goods. When Grigg’s model TEA is implemented, Alice will also pass an entry as a receipt of the transaction in the shared or distributed ledger with her signature. When the transaction becomes visible to Bob, he must also sign the receipt to approve the transaction in the shared ledger. By signing the transaction, Alice and Bob endorse it, and then it becomes part of an immutable ledger. Neither Alice nor Bob can deny or alter the transaction because the transaction in their respective books is also reflected in the shared ledger.

Blockchains for Accounts, Finance, and Audit—The use of distributed ledger technology such as blockchains and financial technology (FinTech) in accounting and finance has led the emergence of another viable accounting system known as TEA.26 TEA represents an innovative and more effective approach to addressing the fundamental problems of trust and accountability inherent in the current accounting model. Although blockchains may appear futuristic, they are based on three technologies: the internet, private key cryptography, and a protocol governing incentivization. These three technologies work together to create a secure system that enables interactions between two parties without needing a third party to facilitate digital relationships. A blockchain can also be called an alternative ledger. A TEA model using a smart contract is also discussed in the study, in which two parties settle terms and conditions and digitally sign a self-executing digital contract on the distributed ledger. Party A agrees to pay $100 to party B for some services. They sign a contract on the distributed ledger. Once the services are delivered, both parties again sign a contract, and party A pays $100 to party B for the services. The author also presented a case study of three real-world TEA and blockchain-based solutions (Luca+, zkLedger, and Pacio), and their respective technical issues were also discussed. Here is a brief discussion:

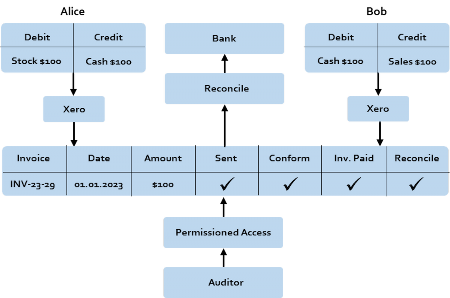

Luca+ by Ledgerium is a BaaS (Blockchain-as-a-Service) model based on TEA and the Ledgerium Blockchain.27 This public ledger facilitates businesses’ ability to record their invoices and payment-related transactions securely. Luca+ is based on the Ledgerium Blockchain and smart contracts, and Ethereum is the underlying platform.28 Luca+ ensures increased trans- parency and accountability, ultimately reducing fraud risk and errors. The key considerations while developing Luca+ were blockchains’ privacy concerns and scalability issues. The public verifiability of a transaction reveals the contents of that transaction, even if it requires verifying a transaction by the auditors. So far, scalability issues in blockchains are the main hurdle to adopting them on a large scale. Luca+ records the third accounting entry on the public ledger via Xero, which is integrated with the application. This entry is passed as proposed by Grigg in his white paper and is conceptually and practically different from the Esersky and Ijiri models. The conceptual working model of Luca+ is explained in Figure 7.

Fig. 7. Luca+ working model.

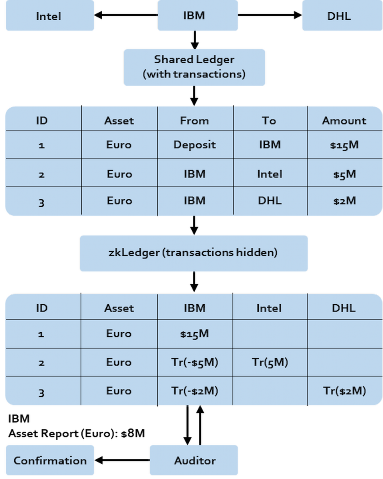

zkLedger by MIT Media Lab is a blockchain-based accounting system with a privacy focus that was created to offer organizations a safe and transparent way to record their financial transactions while protecting the privacy of their sensitive data.29 The zkLedger system uses zero-knowledge proof (ZKP) technology to ensure that financial transactions remain hidden while being confirmed on the blockchain. The system may validate a transaction using ZKP without disclosing private information or the parties’ identities. zkLedger can offer a highly secure and private accounting solution to various enterprises, including those in the financial, healthcare, and legal fields, by combining blockchains and ZKP technology. With permissioned blockchains, zero-knowledge proofs, and additively homomorphic commitment algorithms, zkLedger can produce a verifiable, tamper-resistant ledger of transactions that conceals transaction amounts, senders, and receivers while allowing full audit. Figure 8 depicts the working of zkLedger.

Pacio by Pacio Core Ltd. is a blockchain-based solution that aims to revolutionize the accounting industry by providing a secure, transparent, and efficient method for businesses to record financial transactions.30 Pacio utilizes a private blockchain infrastructure and smart contract technology to create a triple-entry accounting system, which adds a layer of verification to traditional double-entry bookkeeping. Like Luca+ and zkLedger, scalability issues are preventing the mass adaptability of blockchains in the accounting, finance, and auditing domains. Pacio targets the scalability issues of blockchains and aims to address such issues and work on standardizing and simplifying the operations and adaptability of inter-blockchain operations. Pacio is also working to interlink various TEA-based applications into a single stream.

Fig. 8. zkLedger working model.

In his “Financial Accounting in the Era of Blockchain,” Emon Chowdhury stated that organizations could use blockchains to freely publish their financial data quickly to lessen the likelihood of fraud and inaccuracy.31 The author urged accountants, financial regulators, and auditors to use blockchain-based accounting systems to reap the benefits of the accounting ecosystem. The organizations would publish their financial data on a distributed ledger accessible via smart contracts. Any modifications to operational procedures or policies could be recorded on a blockchain. Multiple parties could function as miners not only for rewards but also for readily accessible corporate data. Legal and audit firms could become blockchain nodes. The regulators and the stock exchange would become the nodes of the accounting chain to improve system performance and oversight. The author concludes that implementing blockchains in the accounting ecosystem would be highly beneficial but challenging, and it would take time to materialize the expectations. The study also pointed out various challenges to the adoptability of blockchains in financial accounting. The author insisted that an organization with a huge number of transactions would be a poor fit for implementing a blockchain-based solution because of the huge upfront cost, lack of technical information, and lack of data transparency due to the public nature of blockchains and 51% attacks. The author also highlighted some short-run and long-run benefits of the adoption of blockchains, like transactions being fully transparent, accessible, perfectly traceable, and immutable, and cross-verification of information being quite easy at times of uncertainty, before entering into a big business deal, or before taking big decisions. Likewise, disclosure of information by investors and businesses may also be beneficial for increasing trust, and lowering the cost of trust has some long-run advantages.

In their study, “Toward Blockchain-Based Accounting and Assurance,” Jun Dai and Miklos Vasarhelyi proposed a simplified blockchain-based Triple-Entry Accounting and assurance ecosystem that uses TEA, operates independently, processes data, and generates financial reports.32 The authors stated that TEA is a relatively new approach for recording transactions that require a transaction processing authority to authorize the transaction. As a result, once a transaction is entered, it becomes immutable, and there is no chance of altering or deleting it. Additionally, the smart contract facilitates the fast completion of transactions and allows quick verification. In the proposed ecosystem, when a company purchases goods on credit, it records the transaction in its ERP system. It sends an accounting token to two blockchain accounts, corresponding ERP accounts, for recording and tracking purposes. The blockchain accounts act like a cryptocurrency wallet with a unique ID, complete details of previous transactions for that particular account, a running account balance, and a cryptographic key for transaction verification. The mechanism for recording the transactions is hierarchical. The company is at the top level, then the accounting equation or accounts grouping, assets, liabilities, and equity. All accounts correspond to the third level’s respective balance sheet group items. The balance sheet equation can be validated using a smart contract. The assets are equal to liabilities and equity; if the equation is not balanced, it triggers an alert. As the credit purchases are an obligation for the payment to the suppliers, an obligation token is generated and sent to the blockchain to record this event. This token is for an automated confirmation that the token’s value matches the account receivable balance in the supplier’s books. The obligation token would be implemented through a smart contract and executed for payment once the agreed terms and conditions are realized, such as the payment due date. The ecosystem has downsides, such as the system’s suscepti- bility to cyberattacks and malicious data modification. The authors conclude that blockchains have the potential to improve performance and dependability, which will increase confidence in blockchain-based TEA systems.

In their article, “Blockchain and its Implications for Accounting and Auditing,” Enrique Bonsón and Michaela Bednárová seem convinced that, in the coming years, blockchain technology will have a deep impact on businesses and society as a whole.33 The research study draws on previously published literature to highlight blockchain insights on the transformation of accounting practices. For auditing, automation, and reliability with low-cost and error-free transactions, the author emphasized using a private blockchain for accounting and auditing. With the adoption of blockchains, such as Distributed Consensual Accounting Records (DCAR), smart audit procedures, and blockchain-based TEA, the continuous accounting and auditing process has taken on new dimensions. Blockchains have an advantage over conventional ERP and database management systems due to their immutability, consensus, decentralization, and encryption. According to the study’s findings, blockchains have the potential to completely change accounting and auditing, particularly for continuous audit and financial reporting.

In “Blockchain and Accounting Fraud Prevention: A Case Study on Luckin Coffee,” Tianhao Chen highlighted a fraud case study at Luckin Coffee and advocated the role of a blockchain-based fraud triangle through which fraud could have been identified.34 The author discussed the Fraud Triangle model as it has three key aspects: 1) motivation, 2) opportunity, and 3) rationalization, and explains that they can be overcome with the help of the blockchain-based fraud triangle model, which is essential in preventing fraud. The author suggested the following considerations to break the fraud triangle:

The motivation for fraud can be encountered with the help of decentralizing data instead of having it available in a centralized place.

Blockchains can minimize opportunities for fraud due to their append-only feature. This feature is very helpful in transaction tracking, and any alteration in data with the intention of fraud becomes impossible.

Rationalization becomes impossible by automating the processes using smart contracts because human involvement can be eliminated from the processes and controls.

Chen raises a valid concern about privacy in blockchain-based applications due to the highly transparent nature of blockchains. It is further suggested that with the help of the ZKPs protocol, privacy-related issues can be addressed, as data validation can be done without sharing.

In Tyrone Carlin’s view, given in the article “Blockchain and the Journey Beyond Double- Entry Accounting,” the systems for keeping accounting records before the DEA were not appropriate or usable in the present context of bookkeeping.35 As suggested earlier by Ijiri in 1982 and 1986, the lack of adoption of TEA indicates a greater possibility that TEA will underlie a journey beyond the double entry. While it is impossible to predict to what extent or when it will occur at this time, the possibility of such a transformation creates favorable conditions for establishing in-depth research with global implications. The author admitted that this topic appears to have received comparatively little attention from accounting scholars. Yet a shift beyond DEA and into the era of blockchain-based record keeping will have far-reaching implications for so many facets of financial reporting, management accounting, and auditing, as well as for accounting. While DEA gained popularity gradually over many centuries, it seems improbable that it will hold its current position for a longer time if the blockchain technology lives up to its transformative potential and accounting practices switch towards the TEA modalities. To seize a crucial window of opportunity for influence, engagement, and impact, scholars must focus on the substantial unresolved problem set associated with this transformation. The author suggests that scholars must look forward to creating educational frameworks that will sustain the accounting and auditing professions into the era beyond double-entry bookkeeping.

The transition from DEA to TEA is only a matter of time, according to the authors of the article “Blockchain Hash, the Missing Axis of the Accounts to Settle the Triple Entry Bookkeeping System,” who examined how blockchains can provide an important advancement in audit control functions.36 The term “ledger” in blockchain is derived from accounting, and in order to complete the TAccounts, the third part of the transaction must be included to make it into an X-shaped format. The third part would be a hash, which would be used as a unique identifier for a transaction. The authors concluded that it is necessary to have two independent methods of verifying every transaction because the evolution of accounts into new forms is unavoidable. By double-checking both ends of the transaction, we can be sure that everything is in order with the DEA. The authors reiterated that an intermediary is required to authenticate the integrity of blockchain data. Participants should use an authentication system to complete the task in their absence.

An investigation of the emerging literature on the topic states that blockchain implementation may result in some significant benefits.37 Through a literature review, Alessio Faccia and Pythagoras Petratos examined whether, if blockchains are integrated into AIS and ERPs, it can produce better services and audit compliance. In this case study, the authors analyze an e-procurement system and its operations and select the SAP ERP system. The authors suggested additional processes to record the combined data, such as hashes, smart contracts and a shared ledger, to facilitate a blockchain-based procurement system. SAP provides a cloud-based platform, “SAP Ariba,” for buyers and sellers, and procurement in the SAP ERP system is routed through MM, SCM, and FI modules. The authors are convinced that shifting to a dedicated procurement platform is highly desirable for many reasons. Some of the advantages highlighted by the authors are that this integration can shorten procurement time and overall improvement in efficiency, reduce procurement cost, ensure security and reliability, and provide a flexible and up-to-date procurement platform. The authors also discussed cloud security, fraud, and access management issues. They concluded that DL, decentralized finance (DeFI), and FinTech applications could facilitate the integration of AIS and ERP systems for an e-procurement system and yield significant benefits.

In “REA, Triple-Entry Accounting and Blockchain: Converging Paths to Shared Ledger Systems,” the authors examined the Resource-Event-Agent (REA) framework to understand how REA influenced TEA, leading to the emergence of distributed ledgers.38 The REA accounting model was proposed by William E. McCarthy in 1982.39 REA is a generalized accounting concept of how accounting practices can be reengineered for AIS. In the REA model, there is no concept of debit and credit. Computers generate real-world objects. The study investigates a genealogical analysis with the mandate to trace the emergence of REA, TEA, and blockchain as shared ledgers. REA accounting and blockchain-based TEA improved traditional accounting and challenged it at many levels. REA, in general, is a framework to establish the ontology, whereas TEA is considered an implementation of REA. But REA has a concept that is functionally the same as TEA. This is the Open-edi Distributed Business Transaction Repository (OeDBTR), which is an ISO/IEC standard for electronic data interchange. TEA is only used for transactions between entities. The REA ontology gives the term OeDBTR to a system that tracks and records the history of the events that cause changes in multiple business entities and relies on an independent view of the transactions as a single source of truth. The ability to maintain multiple views of the same transaction from various locations without compromising the integrity of the record is a key feature that both TEA and OeDBTR share. Despite being a significant step forward, the author argues that the shared ledger is not the ultimate solution because neither DEA nor conventional bookkeeping methods are likely to be replaced anytime soon. A shared ledger can be beneficial for preventing fraud and money laundering, but a shared ledger cannot do this on its own. They provide direction and guidance for making accounting and finance more effective and transparent. The REA model is surrounded by those real-world objects, and they are classified as follows:

Resources: goods, services, and money

Events: transactions that affect resources

Agents: people and businesses

Finally, in “Blockchain Technology in the Future of Business Cyber Security and Accounting,” Sebahattin Demirkan, Irem Demirkan, and Andrew McKee looked at the impact of blockchains on auditing from differing viewpoints and concluded that blockchains would change the auditing profession altogether.40 The authors concluded that implementing blockchains in accounting with cybersecurity in mind will allow transactions to be processed, checked, and measured without the involvement of a third party. That will be the ultimate shift from bookkeeping to TEA. The study also looked into the current and prospective cybersecurity implementations for blockchains and concluded that various aspects of cybersecurity and accounting could be efficiently addressed using blockchain technology.

Blockchains, Trust, and B2B Business—Blockchain-based technologies provide new methods of organizing information that enable complex sociotechnical systems to share information while ensuring the integrity of the information.41 However, as we have seen, there are some potential challenges. Some of blockchains’ essential characteristics prevent upscaling to a global blockchain-enabled information-sharing model in the B2B business. The study “Developing Large Scale B2B Blockchain Architectures for Global Trade Lane” raises scalability issues for blockchains concerning B2B transactions and presents a case study of Global Trade Digitization (GTD) architecture. The blockchain-based GTD was designed for sharing supply chain informa- tion that allows all parties in global supply chains to share data and documents in a trusted and secure manner, and is the first large-scale global blockchain-enabled infrastructure of its type. MAERSK, the largest supply chain company, and IBM, an IT company, jointly developed GTD for the global-scale digitization of international trade.

MAERSK is supposed to process a huge volume of data, and millions of parties are to be identified. It becomes a huge challenge when the data is processed in the logistics B2B domain on a blockchain. A permissioned blockchain architecture in GTD was kept simple and easy by retaining only the hashes and the document itself and offloading the documents to a different installed base. Only limited numbers of nodes were added to the blockchain to keep it less heavy. The validation of the documents was done on a different platform. In GTD, the privacy and confidentiality of the data in B2B were in focus. The authors of the study concluded that international trade domain services are an inspiration and they believe that the identified issues in the GTD’s case study on scalability issues are potentially useful in other domains and B2B businesses. Scaling issues have surfaced as the blockchain is still in its early stages. Based on the study, the authors are convinced that overcoming the stability issues of blockchains could also benefit the B2B business model.

Sara Rouhani and Ralph Deters highlighted the importance of trust in their research, stating that the lack of trust prevents wide-scale data sharing.42 Data owners are reluctant to share their data, and data users are worried about the accuracy of the data due to the non-availability of transparent sharing infrastructure. Data trust in an environment that promotes data sharing and requires data users to use data transparently. The authors propose an end-to-end data trust framework that allows data owners to share their data and users to use it safely. The framework consists of two components: a trust model to analyze the quality of input data, and security and traceability to control and manage data access. The proposed model was successfully implemented using Hyperledger Fabric and then evaluated, producing the desired results. In the study, blockchains were tested and found to be a trusted technology to build and maintain a trustworthy relationship between the concerned parties.

Blockchain technology has become more popular over the past few years because it can create a decentralized and secure digital distributed ledger making data manipulation difficult. Blockchain is a useful tool for financial accounting because it makes it easy and safe to keep track of and record financial transactions. In conventional accounting systems, the financial data is stored on centralized location and controlled by a single entity. This creates a risk of fraud, errors, data breaches, and a lack of accountability and transparency. Blockchains, distributed ledgers that the nodes on a network maintain, address issues of accountability and transparency and have a strong resistance to hacking and data manipulation. One of the key advantages of using blockchains in financial accounting is the ability to create transparent and auditable ledgers of financial transactions. Before being added to the chain, multiple network nodes verify and approve each transaction, and a transaction log is also created. Additionally, blockchains enable real-time monitoring of financial transactions, which can improve financial reporting and decision-making. Since all transactions are recorded on a distributed ledger, authorized parties have real-time access to the information, which can reduce delays in financial reporting and improve the accuracy of financial data. There is increased adoption of blockchains in financial accounting, which can enable faster, more secure, and more transparent financial transactions. Blockchains, as distributed ledgers, can support a permanent and immutable record of all transactions, which can be audited and traced back to their origin, improving transparency and reducing the risk of fraud. Accounting processes can also be automated with the help of blockchains, such as the reconciliation of accounts, inventory tracking, and managing invoices and payments, which can improve efficiency and reduce labor work significantly.

Table 1. Literature Summary.

Study | Trust and Security | Technical Scalability Standards Regulatory Others |

✓ | ✓ | |

✓ | ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ ✓ ✓ | |

✓ ✓ ✓ ✓ | ||

✓ ✓ | ||

✓ | ✓ ✓ ✓ ✓ ✓ | |

✓ | ✓ ✓ ✓ | |

✓ | ✓ ✓ ✓ | |

✓ | ✓ ✓ | |

✓ | ✓ |

Smart contracts on blockchains could be used for various financial transactions due to their secure and transparent execution. Interoperability issues can also be addressed with the help of blockchains as technology continues to evolve, and we can expect to see more widespread adop- tion and integration of blockchain-based applications in financial accounting. Some combined qualitative and quantitative features of blockchains and TEA are summarized in Table 2.

Table 2. Combined Features of Blockchains and TEA.

Aspect | Qualitative Approach | Quantitative Approach |

Accuracy | Increased transparency and reduced chances of error and fraud26 | |

Reliability | Increased trust between stakeholders due to its security features35 | |

Auditing | ||

Security | ||

Overall Benefits | Potential for increased accuracy, reliability, | Increased transparency and trust between |

security, and reputation in financial | stakeholders and reduced likelihood of |

DEA, the underlying accounting method in AIS that has been used for centuries, covers all aspects of bookkeeping. In B2B business mode, when two parties enter into a business deal, they record transactions in their respective books, and there are chances of errors and misrepresentation. There is no coordination or cross-verification between the parties, which may lead to the parties becoming untrustworthy for many reasons. In this scenario, we see that the DEA lacks here. 10 Again, it is not the fault of the DEA, but the advancement in technology, the high volume of transactions, and the growth of business demand determine the DEA’s limits. 15 The three-entry accounting model with a blockchain as a shared ledger could be a choice but also seems vital for safe, secure, and trusted B2B transactions. If the blockchain-based TEA model is applied to accounting and financial systems and AIS using ERP systems, it will help improve traditional accounting cycle standards, offer cost savings, and ensure business transactional security.26 Some key features of Double-Entry Accounting and blockchain-based Triple-Entry Accounting are summarized in Table 3.

Table 3. Comparison of Double-Entry Accounting and Blockchain-based TEA.

From the existing literature on the TEA method, we have included three key authors who presented the concept of triple-entry bookkeeping differently. Consequently, each concept proposed radically different systems in different historical and geographical contexts.

Fedor Esersky’s model was focused on developing a new standard for accounting, the “Russian Triple Entry” (RTE) system.24 He suggests in his proposed model that a transaction be recorded in three accounting books in chronological order immediately after completion. According to his model, the purpose of the third entry is not to make bookkeeping secure and transparent but to gauge the real-time health of the business. DEA is based on pre-defined accounting periods, and after the completion of an accounting period, it is possible to determine the overall condition of the business; there is no way to know it between the accounting periods. Various factors collectively affect the business, and their timing matters, so it is important to know the real-time view of the business. The concept of RTE contradicts the understanding of TEA models presented in recent years. It seems that Esersky wanted to develop better standards for bookkeeping; no particular areas were targeted, and security and privacy were not his concerns. As previously stated, it looks more appropriate to tag Esersky’s work as “Triple-Book Entry” than “Triple-Entry Accounting.”

The Triple-Entry Bookkeeping (TEB) model presented by Yuji Ijiri was not the same as that by Esersky.17, 25 Still, one thing can be seen in both theories: both address bookkeeping collectively, talk about an overall improvement in the processes, and have the same understanding that DEA is not capable enough to present the real-time picture of a business. DEA is limited to debit and credit; therefore, any new dimension to record a third entry might be logical but not physical. He stated that “the rate at which the income is being earned” or, equivalently, “the rate at which the wealth is changing” should be called momentum. He called his model “momentum accounting.” He named the third accounting entry “tribit.” The author, for sure, is convinced that the third entry is essential to a record in that it presents the real-time output of a transaction in financial terms. This model aims to improve accounting procedures and processes while security, privacy, or witnessing transactions are out of the question. The proposed entry has nothing to do with the conceptual workings of blockchains or shared ledgers and does not support the third entry as a witness entry in a distributed or common ledger. The study became a groundbreaking theory, reiterating the concept of three accounting entries without any connection with any of the features of a blockchain.

Table 4. Advantages and Limitations of Blockchain-based TEA.

Advantages |

Limitations |

Improved transparency: Blockchain as DL provides a high level of transparency, can prevent fraud, provides a full audit trail of transactions, and ensures compliance with regulations.18, 31, 34, 36 | Technical complexity: Blockchains are relatively new and, so far, have been implemented in cryptocurrencies only; for other domains and areas, it still requires knowledge and expertise.26, 31–34, 37, 38, 41, 42 |

Reduced cost: In blockchain-based systems, there is no need for any intermediary parties, which can reduce transaction and maintenance costs significantly.31, 33, 40, 41 | Regulatory issues: Legal and regulatory issues surrounding blockchains are still evolving and creating uncertainty for businesses and inventors.32, 34, 35, 37, 40 |

Enhanced security: The algorithms used in blockchains make sure the transactions are secure and temper-proof, and they protect sensitive information. | Integration: Integration with legacy systems is still a big challenge because legacy systems haven’t been updated to work with blockchains yet.18, 26, 31–34, 37, 38, 2640–42 |

Streamlined processes: Blockchains can make it possible to automate manual processes like recordkeeping and account reconciliation, which can reduce errors while saving time and resources.27, 29, 30 | Scalability: The current blockchain infrastructure is not strong enough to handle the current volume of transactions around the world.26, 37, 41 |

Faster transactions and settlement:

Blockchain-based system can manage and process transactions and settlements quickly and shorten lengthy settlement | Lack of standardization: Currently, there are no defined standards for a wide range of industries for blockchain implementation; therefore, businesses are reluctant to adopt this technology.32, 35, 37, 38 |

Grigg presented an innovative concept of Triple-Entry Accounting (TEA) that is more viable and doable than the model presented by Esersky and Ijiri.17,18, 24 The author was focused on a particular area: the recording of transactions that require security, privacy, and witness entries. Like the two earlier models, they presented their so-called solutions for overall bookkeeping, while Grigg’s model was particular to the B2B business model. Coincidentally, the aspects covered in this model are available in blockchains. Some researchers believe that the key motivation behind the blockchain innovation was Grigg’s TEA model, which he defines as “recordkeeping for two or more parties through a shared transaction repository (STR) with a signature by all parties.” Grigg focused on the external transactions outside of the business and put the security and privacy of the data at the top. Table 4 summarizes the advantages and limitations of blockchain-based TEA with regard to their implementation in B2B business.

In this study, we highlighted the key issue in AIS, which is the lack of trust in the B2B business model due to the limitations of DEA. These limitations deal with some unexpected situations such as lack of trust, recording the witness, or three-entry accounting phenomena that did not surface when defining the DEA rules. As of now, DEA is still in place, and there is no doubt about its viability, capacity and integrity. Blockchain technology is an innovative solution with the potential to transform financial accounting altogether and can increase the accuracy, efficiency, and transparency of financial transactions. Financial transactions can be recorded transparently and immutably, ensuring that all parties have access to the same information. It reduces the chances of errors and fraud and increases trust between parties. In addition, Blockchain can automate many manual processes, such as reconciling transactions and confirming the authenticity of financial documents. It can significantly reduce processing time and other time-intensive tasks, thereby saving time and money. Real-time visibility into financial data is also possible, which can help businesses make informed decisions and respond quickly, which could provide investors with accurate financial information promptly to make investment decisions.

Future Directions—It is strongly recommended that new research be carried out to highlight and reap the potential of blockchain-based distributed ledgers for TEA implementation, particularly in accounting and finance. Blockchain technology could create a trustworthy and safe environment for businesses, but this will require time and considerable research. Future research should focus on developing best practices and standards to implement blockchains in accounting and finance while addressing security, technical, scalability, standardization, the regulatory framework, scalability, integration, and complexity issues.

All authors contributed equally to this research study.

The authors affirm they have no conflicts of interest as described in journal’s Conflict of Interest Policy.

1 Desai, S., Deng, Q., Wellsandt, S., Thoben, K.-D. “An Implementation of IoT-Based Product Tracking with Blockchain Integration for a B2B Platform.” In Proceedings - 2020 IEEE International Conference on Engineering, Technology and Innovation (ICE/ITMC), June 15-17, 2020, Cardiff, United Kingdom (IEEE) 1–8 (2020) https://doi.org/10.1109/ICE/ITMC49519.2020.9198639.

2 Eid, R., Trueman, M., Ahmed, A. M. “B2B International Internet Marketing: A Benchmarking Exercise.” Benchmarking 13.1/2 200–213 (2006) https://doi.org/10.1108/14635770610644682.

3 Mazur, M. “Blockchain-Powered New Generation of Global B2B Platforms: A Conceptual Approach.”SSRN Electronic Journal (2020) (accessed 05 October 2022) https://doi.org/10.2139/ssrn.3678563.

4 Sangster, A. “The Genesis of Double Entry Bookkeeping.” Accounting Review 91.1 299–315 (2016) https://doi.org/10.2308/accr-51115.

5 Sarwar, M. I., et al. “Data Vaults for Blockchain-Empowered Accounting Information Systems.” IEEE Access 9 117306–117324 (2021) https://doi.org/10.1109/ACCESS.2021.3107484.

6 Bendovschi, A. C. “The Evolution of Accounting Information Systems.” Digital Accounting III.I(7) 91–96 (2011).

7 Daoud, H., Triki, M. “Accounting Information Systems in an ERP Environment and Tunisian Firm Perfor- mance.” International Journal of Digital Accounting Research 13 1–35 (2013) https://doi.org/10.4192/ 1577-8517-v13_1.

8 Basu, S., Waymire, G. “The Evolution of Double-Entry Bookkeeping.” SSRN Electronic Journal (2021) (accessed 09 October 2022) https://doi.org/10.2139/ssrn.3093303.

9 Maiti, M., Kotliarov, I., Lipatnikov, V. “A Future Triple Entry Accounting Framework Using Blockchain Technology.” Blockchain: Research and Applications 2.4 1–8 (2021) https://doi.org/10.1016/j.bcra. 2021.100037.

10 Fraser, I. A. M. “Triple-entry Bookkeeping: A Critique.” Accounting and Business Research 23.90 151–158 (1993) https://doi.org/10.1080/00014788.1993.9729872.

11 Sarwar, M. I., Nisar, K., Khan, A. “Blockchain - From Cryptocurrency to Vertical Industries - A Deep Shift.” In Proceedings - 2019 IEEE International Conference on Signal Processing, Communications and Computing (ICSPCC), September 19-21, 2019, Dalian, China (IEEE) 1–4 (2019) https://doi.org/10.1109/ICSPCC46631.2019.8960795.

12 Nakamoto, S. “Bitcoin: A Peer-to-Peer Electronic Cash System.” (2008) (accessed 04 August 2018)https://bitcoin.org/bitcoin.pdf.

13 Sarwar, M. I., Nisar, K., Andleeb, S., Noman, M. “Blockchain - A Crypto-Intensive Technology - A Review.” In Proceedings - 35th International Business Information Management Association (IBIMA) Conference, April 1-2, 2020, Seville, Spain (IBIMA Publishing) 14803–14809 (2020) https://ibima.org/accepted-paper/blockchain-a-crypto-intensive-technology-a-review.

14 Carruthers, B. G., Espeland, W. N. “Accounting for Rationality: Double-Entry Bookkeeping and the Rhetoric of Economic Rationality.” American Journal of Sociology 97.1 31–69 (1991) https://doi.org/10.1086/229739.

15 Williams, J. J. “A New Perspective on the Evolution of Double-Entry Bookkeeping.” The Accounting Historians Journal 5.1 29–39 (1978).

16 Capactix “Understanding Double Entry And Triple Entry Accounting.” (2021) (accessed 03 October 2022) https://www.capactix.com/understanding-double-entry-and-triple-entry-accounting.

17 Ijiri, Y. “A Framework for Triple-Entry Bookkeeping.” The Accounting Review LXI 745–759 (1986).

18 Grigg, I. “Triple Entry Accounting.” (2005) (accessed 18 October 2022) http://iang.org/papers/ triple_entry.html.

19 Gröblacher, M., Mizdraković, V. “Triple - Entry Bookkeeping: History and Benefits of the Concept.” In Proceedings - 2019 International Scientific Conference, (Finiz), December 6, 2019, Singidunum University, Belgrade, Serbia 58–61 (2019) https://doi.org/10.15308/finiz-2019-58-61.

20 Ne, I. A. A., Polaka, G., Ruza, O. “Calculation of Financial Indicators in a Single-Entry Accounting System.” Journal of Social Sciences 1.7 17–27 (2015) https://doi.org/10.17770/lner2015vol1.7.1177.

21 Schultz, S. M., Hollister, J. “Single-Entry Accounting in Early America: The Accounts of the Hasbrouck Family.” Accounting Historians Journal 31.1 141–174 (2004).

22 Ellerman, D. “On Double-Entry Bookkeeping: The Mathematical Treatment.” arXiv (2014) (accessed 27 October 2022) https://doi.org/10.48550/arXiv.1407.1898.

23 Ellerman, D. P. “Double Entry Multidimensional Accounting.” Omega International Journal of Management Sciences 14.1 13–22 (1986) https://doi.org/10.1016/0305-0483(86)90004-6.

24 Torrebruno, G. “The ‘Russian’ Triple Entry.” (2020) (accessed 12 August 2022) http://www.alexpander.it/17-RussianTripleEntry.pdf.

25 Platonova, N. V. “FV Ezersky and the Development of Accounting Thought and Practices in Russia.” Vestnik NSUEM (2016) (accessed 03 November 2022) https://nsuem.elpub.ru/jour/article/view/588?locale=en_US.

26 Cai, C. W. “Triple-Entry Accounting with Blockchain: How Far Have We Come?” Accounting and Finance 61.1 79–93 (2021) https://doi.org/10.1111/acfi.12556.

27 Luca+ by Ledgerium. (accessed 22 October 2022) https://www.lucaplus.com.

28 Buterin, V. “Ethereum: A Next-Generation Smart Contract and Decentralized Application Platform.” (2014) (accessed 29 October 2022) https://ethereum.org/en/whitepaper/.

29 ZkLedger by MIT Media Lab. (accessed 13 October 2022) https://dci.mit.edu/zkledger.

30 “PACIO White Paper.” (2021) (accessed 17 October 2022), https://pacio.io/docs/PacioWhitePaper.pdf.

31 Chowdhury, E. “Financial Accounting in the Era of Blockchain - A Paradigm Shift from Double Entry to Triple Entry System.” SSRN Electronic Journal (2021) (accessed 21 November 2022) https://doi.org/10.2139/ssrn.3827591.

32 Dai, J., Vasarhelyi, M. A. “Toward Blockchain-Based Accounting and Assurance.” Journal of Information Systems 31.3 5–21 (2017) https://doi.org/10.2308/isys-51804.

33 Bonsón, E., Bednárová, M. “Blockchain and Its Implications for Accounting and Auditing.” Meditari Accountancy Research 27.5 725–740 (2019) https://doi.org/10.1108/MEDAR-11-2018-0406.

34 Chen, T. “Blockchain and Accounting Fraud Prevention: A Case Study on Luckin Coffee.” In Proceedings - 2022 7th International Conference on Social Sciences and Economic Development (ICSSED), March 25-27, 2022, Wuhan, China 44–49 (2020) https://doi.org/10.2991/aebmr.k.220405.009.

35 Carlin, T. “Blockchain and the Journey Beyond Double Entry.” Australian Accounting Review 29.2 305–311 (2019) https://doi.org/10.1111/auar.12273.

36 Faccia, A., Moşteanu, N. R., Cavaliere, L. P. L. “Blockchain Hash, the Missing Axis of the Accounts to Settle the Triple Entry Bookkeeping System.” In Proceedings - ACM International Conference on Information Management Engineering (CIME), September 16–18, 2020, Amsterdam, Netherlands (ACM) 18–23 (2020) https://doi.org/10.1145/3430279.3430283.

37 Faccia, A., Petratos, P. “Blockchain, Enterprise Resource Planning (ERP) and Accounting Information Systems (AIS): Research on e-Procurement and System Integration.” Applied Sciences (Switzerland) 11.15 1–17 (2021) https://doi.org/10.3390/app11156792.

38 Ibañez, J. I., Bayer, C. N., Tasca, P., Xu, J. “REA, Triple-Entry Accounting and Blockchain: Converging Paths to Shared Ledger Systems.” SSRN Electronic Journal (2020) (accessed 09 October 2022) https://doi.org/10.2139/ssrn.3602207.

39 McCarthy, W. E. “The REA Accounting Model: A Generalized Framework for Accounting Systems in a Shared Data Environment.” The Accounting Review LVII 554–578 (1982).

40 Demirkan, S., Demirkan, I., McKee, A. “Blockchain Technology in the Future of Business Cyber Security and Accounting.” Journal of Management Analytics 7.2 189–208 (2020) https://doi.org/10.1080/23270012. 2020.1731721.

41 Tan, Y., Rukanova, B., Engelenburg, S., Ubacht, J., Janssen, M. “Developing Large Scale B2B Blockchain Architectures for Global Trade Lane: Are the Design Principles Derived Based on the Upscaling of the Internet Applicable for Upscaling Global Blockchain-Enabled Infrastructures?” In Proceedings - 6th Innovation in information infrastructures (III) workshop, 18- 20 September 2019, Surrey, UK 1–8 (2019) .

42 Rouhani, S., Deters, R. “Data Trust Framework Using Blockchain Technology and Adaptive Transaction Validation.” IEEE Access 9 90379–90391 (2021) https://doi.org/10.1109/ACCESS.2021.3091327.

![]()